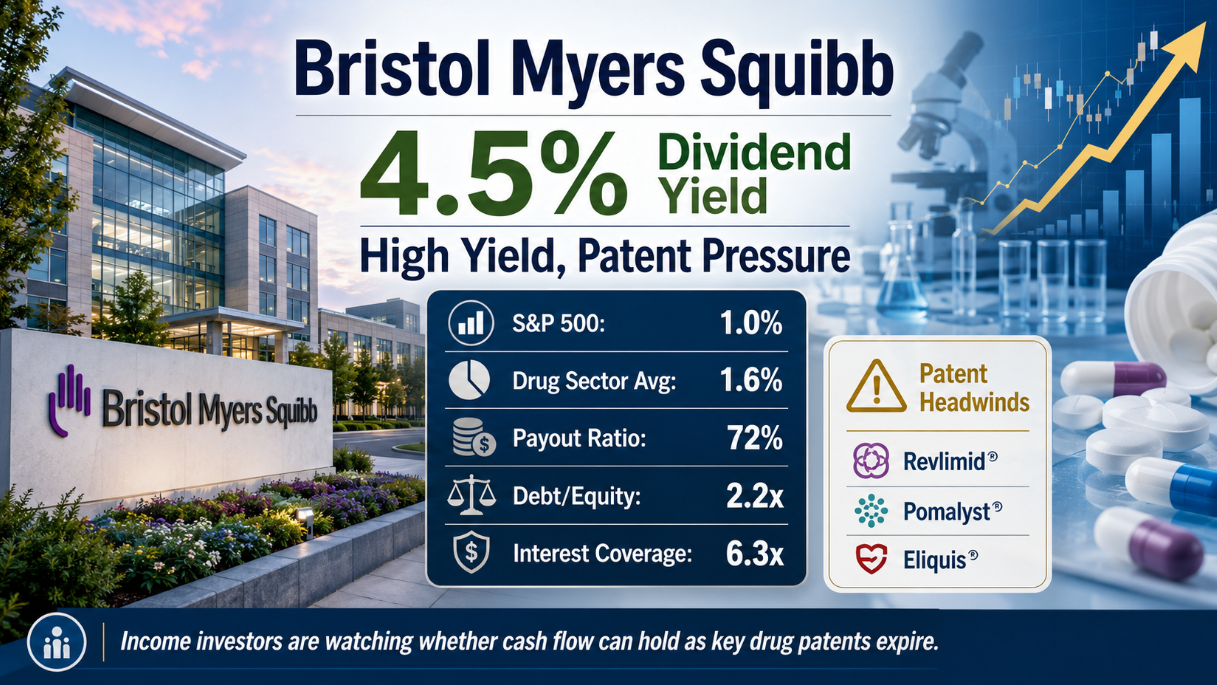

Bristol Myers Squibb is offering investors a dividend yield of 4.5%, well above the 1% yield from the S&P 500 index and the 1.6% average for the drug sector, according to a report by Yahoo Finance.

The yield is drawing attention from income investors, but the company faces real headwinds. Several of its most important drugs are losing patent protection, including Revlimid, Pomalyst, and Eliquis, which is marketed in partnership with Pfizer. Patent losses typically put direct pressure on a company's revenue and earnings, and timing gaps between losing exclusivity and bringing new drugs to market are common in the pharmaceutical industry.

The dividend payout ratio currently stands at around 72%. That is on the higher side but leaves some room before a cut would become necessary. The company has an investment-grade credit rating, a debt-to-equity ratio of 2.2 times, down from 3 times at the end of 2024, and interest coverage of 6.3 times. Those figures suggest the company could take on additional debt to support its business and dividend if needed during a difficult stretch.

Bristol Myers Squibb has a long track record. Its dividend has not been raised every year, but it has trended higher for decades. The board of directors ultimately controls dividend policy, and the history of the dividend suggests the board treats it as a priority for shareholders.

The company is working to develop new drugs to replace lost revenue, but the window between patent expirations and new drug approvals can create pressure on cash flow in the near term. The payout ratio could rise before new products begin contributing meaningfully.

For investors who cannot tolerate uncertainty, the 4.5% yield and the patent headwinds may make Bristol Myers Squibb an uncomfortable fit. For investors who can accept some near-term pressure, the company's financial position, long history, and still-manageable payout ratio offer a reasonable foundation for expecting the dividend to hold.